The Synthetic CIO: How AI Delivers CIO-Level Advice to Every RM in Wealth Management

Fifty relationship managers, one investment philosophy, fifty different answers. What a properly woven AI layer can do to make every RM as consistent as the firm's best one.

7 min read

There is a gap in almost every wealth management firm that no one talks about openly. Not a gap in investment research. Not a gap in the quality of the CIO's thinking. Not a talent gap inside the advisory team.

It is the gap between what the investment committee decides and what the client actually hears.

The CIO and the investment committee spend weeks debating the macro environment, reviewing sector exposures and stress-testing the model portfolio. They arrive at a clear view, put it in a circular, and sometimes run a training session. Then fifty relationship managers walk out to two hundred clients each, carrying their own interpretations and their own bandwidth for preparation on any given morning.

One RM says: maybe move to debt. Another says: hold your asset allocation, markets are volatile. The CIO's view was: focus on capital preservation, capture structural growth, optimise for volatility.

One firm, one investment philosophy, three different answers to the same client question.

This is advice drift. It is one of the most expensive and least-discussed problems in wealth management. Different clients receive different advice on the same market event from the same firm. The firm is no longer running a wealth advisory business; it is running fifty independent advisory businesses under one brand.

Training has a ceiling

The instinctive answer is training. Run better programmes, share the circular more widely, hold weekly investment briefings. Firms do all of this, and it helps to a point. But training hits a ceiling when fifty people have to apply institutional thinking across ten thousand client interactions a month. The ceiling is not the quality of the training. It is the absence of a system that enforces the institutional view in real time, at the point of the client conversation.

The problem compounds in three ways.

Scale is moving in the wrong direction. The wealth industry in India and globally is growing fast, and most institutions are scaling their advisor headcount to capture that demand. The CIO bench cannot scale at the same rate, and trying to train every new RM to senior-PB depth in months rather than years is the kind of programme firms run for years without ever closing the gap. The problem is especially acute in universal banks, where the branch RM is often the first-line wealth advisor for a large mass-affluent customer base. The branch RM does not need to become a CIO. They need a tool that lets them be wiser at the point of advice than their experience alone would allow.

Preparation is the bottleneck, not capability. Industry coverage of advisor time consistently lands in the same place: a large majority of an RM's working week goes to administrative work, data gathering and meeting prep, with a thin slice left over for actual client advice. McKinsey separately projects the US wealth industry will be short 90,000 to 110,000 advisors by 2034 at current productivity levels, roughly 30% of headcount. The arithmetic forces a different question. Not how do we hire more, but how do we get more from the people we already have.

The institutional view is disconnected from the client context. Even when the house view is clear, it lives in a document that is disconnected from the client's actual portfolio. The RM knows the view. They know the portfolio is in some system. Synthesising the two, recognising that this client's equity allocation is 7% above the mandate ceiling, that this is exactly the situation the CIO's current view addresses, and that the recommended action is a specific switch, takes time and depth that not every RM has at 9 AM before the call.

What a well-integrated AI layer can do here

The answer cannot be more training or more head count. It has to be a system that delivers institutional thinking to every client conversation as a default behaviour, not as a special preparation effort. That is the role of a properly woven AI layer inside a wealth platform. The category name for this kind of capability is the synthetic CIO.

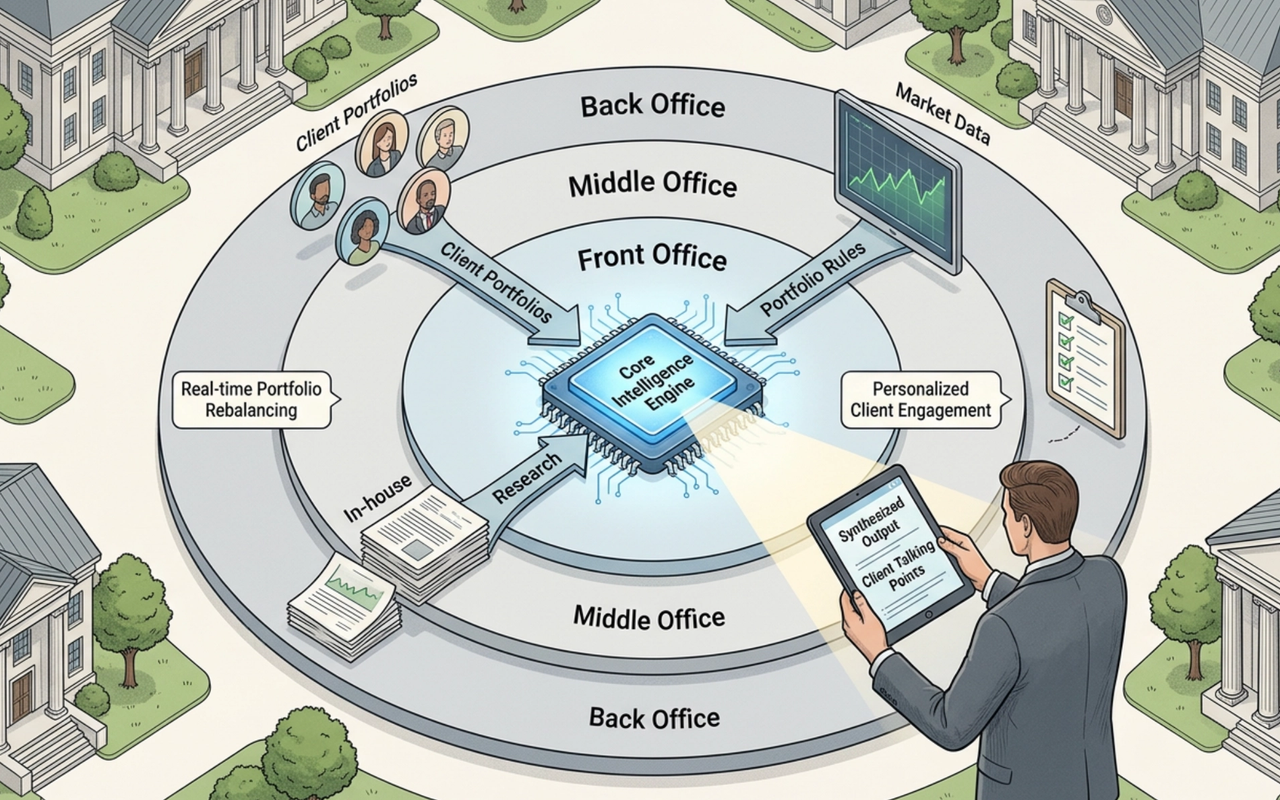

Done well, a synthetic CIO is not a chatbot, not a generic AI assistant, and not a module sold separately. It is an AI layer running on the same data model as the rest of the platform: the same client context, the same portfolio logic, the same mandate rules that govern every other function of the system. Its job is to synthesise everything a CIO-level advisor would consider before a client conversation and surface it to every RM, automatically, before the call begins.

The phrase that matters is blending the client's portfolio with current market context. A generic AI tool can tell an RM what the market is doing. It cannot tell the RM how the market applies to this client: that Priya Sharma's equity allocation is 7% above her mandate ceiling, why that matters given the CIO's current view on large-cap rotation, and what the precise, suitability-checked corrective trade is. A good synthetic CIO does that for every client on every RM's book, every morning, without the RM having to ask.

What the AI actually synthesises

Five inputs run continuously into the layer. All of them should already exist on a well-integrated wealth platform; the work is in synthesising them.

- Portfolio holdings. The real-time picture of every client's invested assets across mutual funds, equities, bonds, alternatives and held-away positions.

- Mandate, IPS and suitability. What the client has agreed to, what their risk profile permits, and what the SEBI suitability matrix allows for their category.

- House view. The firm's current investment positioning, sector tilts, asset class views, tactical recommendations. Entered once by the investment team and applied consistently to every client.

- Market data and news. Live intelligence linked automatically to the holdings in each client's portfolio. A pharma correction surfaces every client with material pharma exposure within minutes.

- Client lifecycle events. Maturing FDs and bonds, approaching SIP renewals, overdue reviews, dropping engagement scores. Every time-sensitive trigger that creates a reason to call.

The output is a single compliance-validated brief per client, surfaced to the RM before the meeting begins.

That is the entire output. Not a data dump, not a dashboard, not "here is everything we know about this client, good luck." A specific insight, a rationale rooted in the firm's current view, a precise action, and pre-cleared compliance. Four lines. The RM does not synthesise. The platform does. The RM delivers the advice.

The RM's day, prioritised

A good synthetic CIO does not stop at preparing advisory briefs. It also determines what the RM should do with their day.

Every morning, the RM sees a prioritised, client-specific action list ranked by urgency, client value and relationship health, and re-ranked through the day as events change. Five triggers move clients to the top of the queue:

- Maturing instruments. FDs and bonds approaching maturity, with reinvestment options pre-computed for the client's risk profile and the current market.

- Market-impacted clients. When a sector moves materially, every client with significant exposure is surfaced automatically.

- Mandate alerts. Portfolios drifting toward a breach are flagged before the breach happens, not at the quarterly review.

- Reviews overdue. Clients past their scheduled review cycle, ranked by AUM and engagement signals.

- Engagement signals. Clients going quiet, with declining logins, missed SIPs or reduced interaction, flagged before silence becomes churn.

This is not scheduling software. It is the system deciding, on behalf of the RM, that the next conversation worth having today is the one with the client whose mandate is about to break.

What changes, by role

CIO and Head of Advisory. The investment view stops being a document and becomes a live input to every RM's recommendation screen. Drift is caught in real time rather than at quarter-end. The strategy is applied consistently across the book, not approximately.

CEO and Head of Wealth. The same advisor team handles a materially larger book, because the prep work that used to fill their week is gone. McKinsey estimates the industry needs to lift advisor productivity by 10 to 20 percent over the next decade just to keep up with demand. Cerulli's data already shows team-based and heavy-tech practices managing roughly three times the AUM of their less-equipped peers. A synthetic CIO is what that capacity looks like inside a single firm.

Compliance and Risk. Every recommendation reaches the client only after passing mandate and suitability checks. The audit trail exists in real time, not at audit. Regulatory readiness is built into the workflow rather than reconstructed before each examination.

What separates AI that works from AI that does not

A fair question: how is a wealth-grade synthetic CIO different from an RM prompting a general-purpose AI tool with a client's situation? The difference is the data it operates on.

| Generic AI tool | Wealth-grade AI layer |

|---|---|

| Separate data model. Knows nothing about your clients. | Same data model as the rest of the platform. Sees every client, every mandate, every position. |

| Generic recommendations with no firm context. | Firm-specific recommendations tied to the house view, the client's portfolio and the active mandate. |

| RM has to copy results into the actual platform. | Lives inside the RM workflow. Surfaced before the call, in the screen the RM already uses. |

| No compliance validation. Creates regulatory risk. | Every recommendation pre-validated against mandate and SEBI suitability before it surfaces. |

| One model wrapped in an "AI-powered" label. | Advisory-specific architecture built into the platform, not a chat layer pasted on top. |

There is a simple test for whether AI is genuinely integrated or just bolted on. Remove the AI layer. Would the platform's core workflows break? If the answer is no, the AI is a feature, not infrastructure. The synthetic CIO concept only works when the answer is yes.

The architecture this needs

A synthetic CIO depends on something most stacks do not have: a unified data model. One codebase across the wealth platform, covering client engagement, portfolio intelligence, advisory, execution and operations. One version of the truth across all of them. The RM sees the same data the client sees. The CIO's model portfolio flows directly into the RM's recommendation screen. Operations sees what was executed. Compliance has a live audit trail.

An AI tool sitting on top of five disconnected systems cannot synthesise five data sources. It can only access what it is connected to. A synthetic CIO works because everything lives in one place. That is also why so many AI advisory features underdeliver elsewhere: the engine is starved of context the platform technically has but architecturally cannot share. The fix is not a smarter model. It is the platform underneath it.

The wealth manager of 2030 is already here

The wealth manager of 2030 will work with a platform that knows the client's risk profile, the current market conditions, and the exact mandate-aware action, drafted before the RM picks up the phone. That is not a prediction. It is what runs in production today, in firms serving anything from boutique advisors to universal banks.

A synthetic CIO does not replace the relationship manager. It makes every relationship manager as prepared as the best one on the floor: consistent, accurate, and delivering the firm's view rather than their own interpretation of it. For firms where fifty RMs give fifty different answers to the same market question, this is not an upgrade. It is what advisory at scale actually requires.

See it come together

How portfolio, house view, mandate and market context assemble into one investor-specific brief, ready before the RM picks up the phone. Valuefy can walk you through it on a real client portfolio.

Request a walkthroughAbout Valuefy

Valuefy is the full-stack wealth management platform, front office to back office, insight to execution. Built by domain practitioners, trusted by 50+ institutional clients across India, GCC, Singapore and Europe, including global private banks, Indian banks and NBFCs, multi-family offices and boutique advisors. Founded by IIM-A and IIT-B alumni with roots in quantitative analytics at Fractal Analytics. $300B+ in assets processed annually. Presence in India, Singapore, Dubai, London, and Switzerland. Wealth. Simplified.