Offering a cloud-based wealth management software platform to serve the needs of modern wealth managers covering the front to back-office

Create personalized experience and operational efficiency with our wealth management software

Our wealth management analytics are adept in modernizing the infrastructure by providing integrated or plug n play solutions.

Integrate

Solve the data challenge across multiple data sets, custodians, brokers, currencies and products. Our wealth management platform aggregates and standardizes data and enables insights.

Automate

Automate the advisory flow and process by automating multiple tasks, including investment policy statements (IPS), mandates, model portfolios and portfolio rebalancing.

Collaborate

Our private wealth management software provides one system to connect small teams and high-profile clients.

Engage

Our wealth platform deploys on the cloud for cost effectiveness, with high-levels of security built-in and compliance with multiple jurisdictions covered.

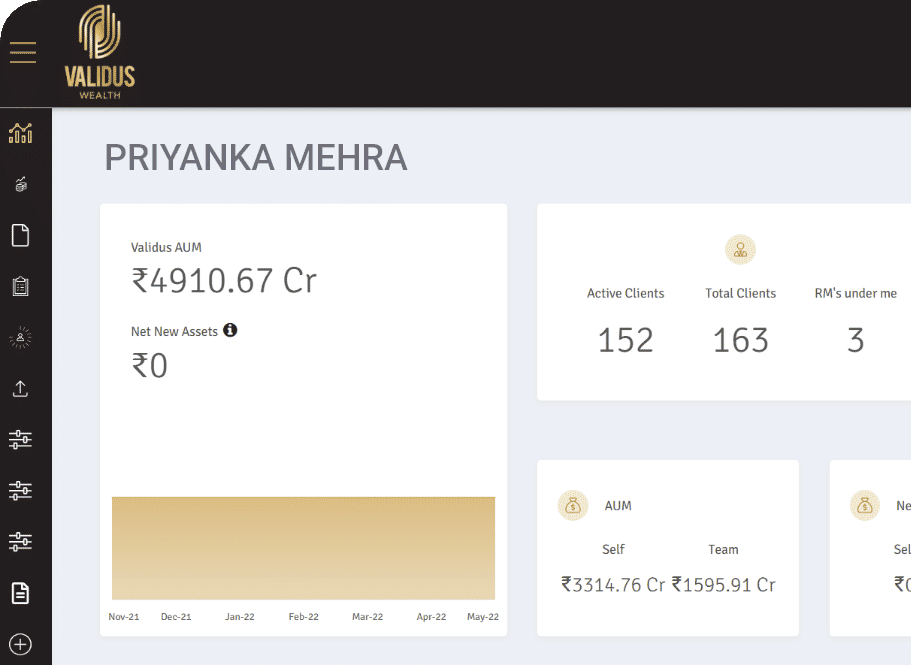

Case Study

Validus Wealth

Evolving with Time

Validus Wealth wanted to further enhance its next generation private client platform by effectively and consistently leveraging the collective capabilities of its 500 talented team members.

View Case Study

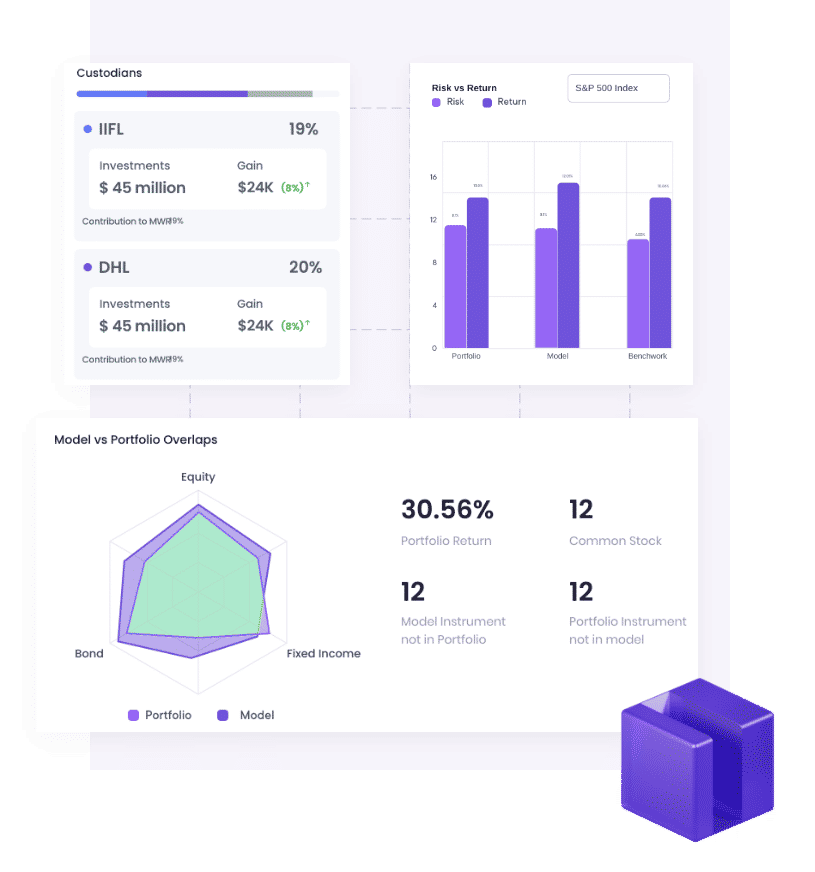

Client Reporting with embedded analytics

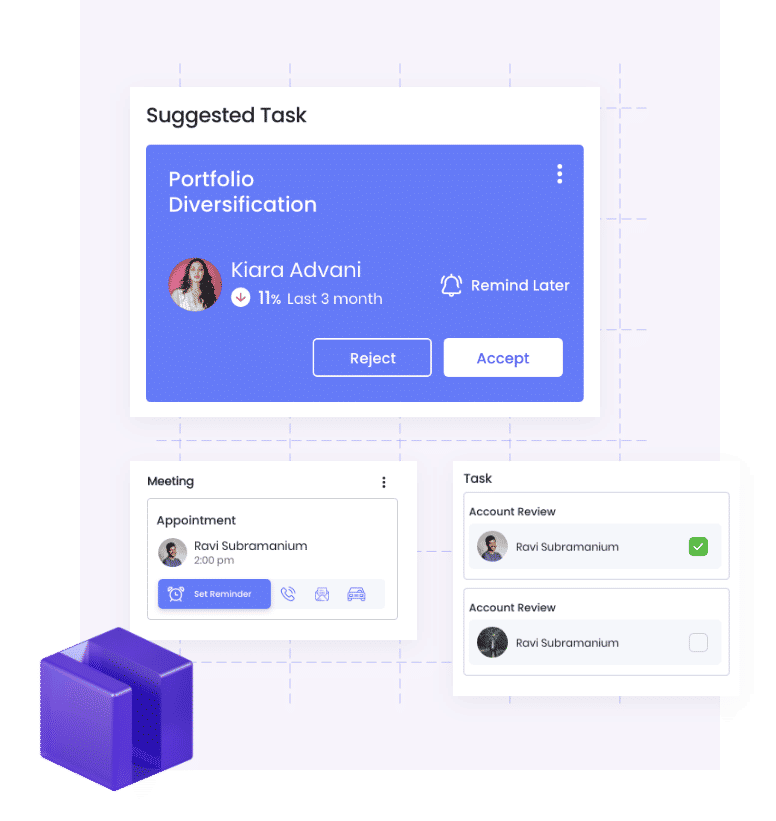

Advisor Workbench

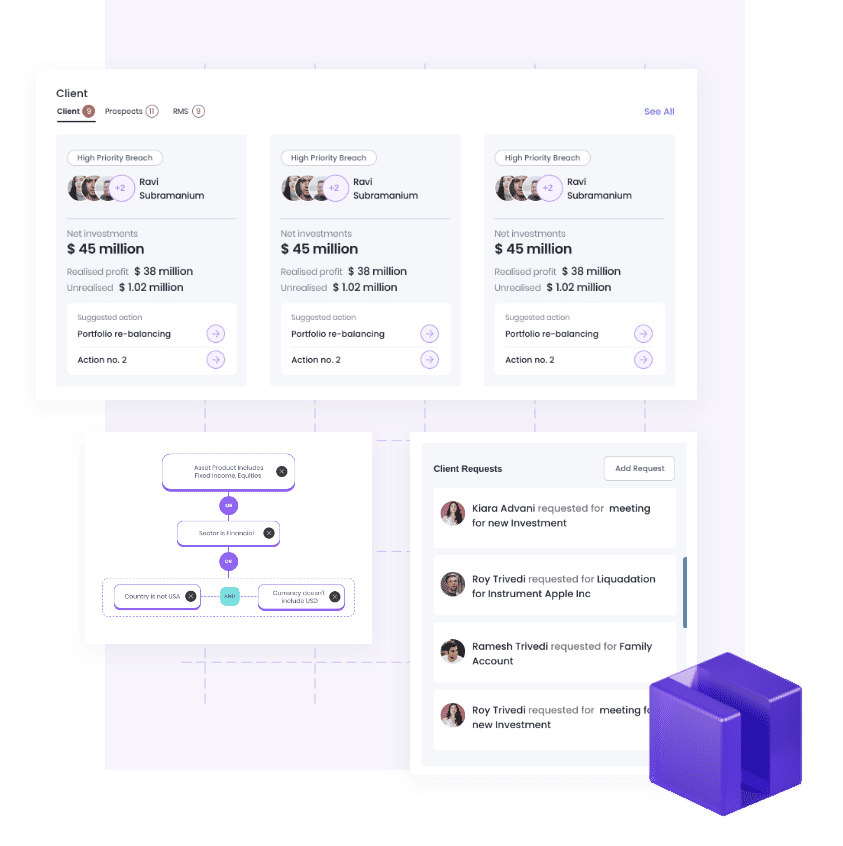

Client Life Cycle Management

Leveraging Valuefy's Wealth in a Box Technology has positioned us for growth alongside the next generation of advisors. By eliminating the complexities of manual processes, we've achieved operational efficiency and enhanced accuracy.

Carol Seah

CEO & Founder, WYNNES Financial Advisers

ITUS acknowledges that Valuefy’s Wealth in a Box Technology platform is instrumental in scaling their business, enabling them to manage larger volumes of assets more efficiently.

BT Chua

Founder and CEO, ITUS Asset Management

Maitri highlights Valuefy’s Wealth in a Box Technology for its customizability, recognizing the unique needs of each Financial Institution, and avoiding a one-size-fits-all approach.

Benjamin Lim

Operations Head, Maitri Asset Management

ZICO believes technology can enhance operational efficiency, They adopted Valuefy's Wealth in a Box Technology in 2021 to enhance and fortify their growth trajectory

Simon Lim

CEO, Zico Asset Management

We chose Valuefy as someone who will take care of our data integration, as someone who will create solution which is customized for us and third party solution we can use to empower our portfolio managers.

Nilesh Shah

Managing Director, Kotak AMC. Ltd.

Valuefy is one such system that we used to automate our process. The platform offers portfolio aggregation services an area that is not well known but is growing.

Kin Onn Kee

Wellfarer Group President and Director

I think the success of any platform is reflected by the usage, the response was uniformly very positive. And till today, the number of logins into the system actually keep increasing every single time.

Parinaz Vakil

Senior Executive Vice President, Digital, IIFL Wealth

The ability to work with a company like Valuefy enables us to bring cutting edge analytics and digital solutions to our clients which was not something that they would have seen or their previous generations would have actually noted.

Soumya Rajan

Founder, Managing Director & CEO- Waterfield Advisors